Lakeland Commercial Property Business Interruption Claims Lawyer

Like residential homes, businesses that get hit by a storm can suffer physical damage and incur significant costs to repair or renovate the structure, replace damaged contents, and remediate affected areas. Commercial property claims can include damage to equipment and inventory as well as the physical structure itself.

Businesses also have a category of damages unique to their character as commercial enterprises, which is business interruption loss. Business interruption represents a tangible loss to companies, and making up for that loss through insurance benefits can be critical to staying afloat while attempting to bounce back and rebuild after a devastating storm. The Ruel Law Firm helps businesses and other entities in Central Florida such as churches, hospitals, apartments, and condominiums with their commercial property claims. If you are having trouble with your property damage claim, our dedicated insurance attorney can help. Call our experienced Lakeland commercial property business interruption claims lawyer today for a free consultation regarding your claims.

How Business Interruption Claims Work

Business interruption coverage is not a standalone insurance policy that one purchases. Typically, it is a term or endorsement that is supplemental to a company’s property or casualty policy, or perhaps its general liability policy. Business interruption coverage is also sometimes called extra expense coverage. When forces outside your control interrupt the flow of your business, business interruption coverage should pay for the financial loss caused by that interruption. The source of the business interruption could be storm damage, fire, vandalism, or any physical damage that keeps you from conducting your normal operations.

Typically, some direct physical loss or damage is required for business interruption coverage to kick in, but it could also apply when the government shuts down the street where the business is located, forcing the business to cease operations during the shutdown. Most policies will require a closure of a minimum amount of time for the coverage to apply, such as a closure lasting 48 or 72 hours, so a one-day closure for a street fair or sewer repairs won’t trigger the coverage, but a more extensive closure might. Insurance policies differ, so it’s important to know the precise terms of your particular policy to know when your business interruption coverage comes into play.

The benefit provided by business interruption coverage is the business income you would have otherwise generated during the period your business is shuttered had you been able to stay open. Benefits could also possibly include increased operating expenses due to the triggering event, such as if you have to incur costs to move to a temporary location, or if you need to continue meeting payroll, paying taxes, and making rent or loan payments during the period your business is closed and not generating any revenue.

The coverage period for business interruption should last through the time necessary to make repairs and reopen, but the length of the period depends on the terms in your policy. For instance, extended coverage will continue to provide benefits after repairs have been made until your income level bounces back to its historical level – depending on the nature of the business, it can take time for customers to return and to build back after an extended closure.

How the Ruel Law Firm Can Help

Business interruption coverage is an essential part of your commercial property or casualty insurance policy; it can be as important or more important than the benefits needed to rebuild a structure or replace damaged equipment. Yet disputes can arise in many ways when it comes to making a claim for business interruption coverage. Some of the most common problems policyholders face include:

- Disputes over the proper calculation of lost income.

- Loopholes in the policy through which the insurer attempts to exclude the loss or covered event.

- Unreasonable, endless requests for documentation from the insured.

- Denial of the claim without explanation.

Florida attorney Michael Ruel spent over 15 years as an insurance defense attorney dealing with commercial property claims before he opened the Ruel Law Firm to represent the needs of policyholders. If your insurance claim is denied, or if you believe it is being unreasonably delayed or underpaid, the Ruel Law Firm can intervene on your behalf and work directly with the insurance company to resolve your dispute. We have extensive litigation experience and are well-equipped to take your case to trial when the matter can’t be resolved outside the courthouse.

Contact the Ruel Law Firm Today

Insurance policies are dense, technical, complex and complicated. Don’t take the insurer’s word for it when they tell you your loss isn’t covered or the amount they offer doesn’t meet your needs. Contact the Ruel Law Firm for a free consultation with a skilled and knowledgeable insurance attorney serving commercial property insurance holders throughout Central Florida. Contact our experienced Lakeland commercial property and business interruption claims lawyer today.

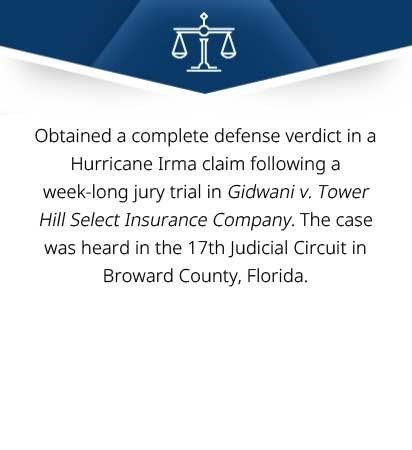

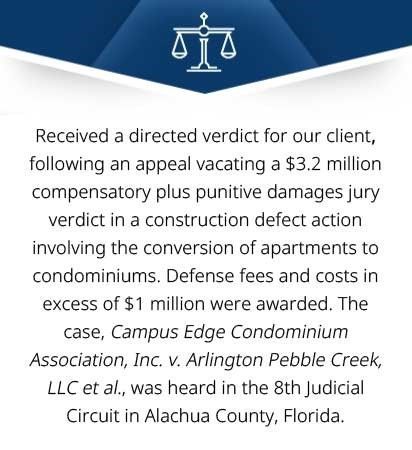

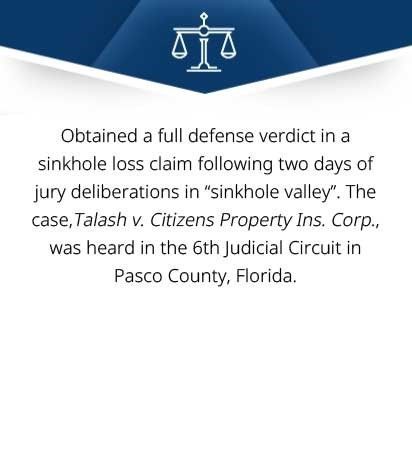

Recent Results

Slide title

Write your caption hereButton

Slide title

Write your caption hereButton

Slide title

Write your caption hereButton

Slide title

Write your caption hereButton

Slide title

Write your caption hereButton

Ruel Law Firm. All rights reserved.